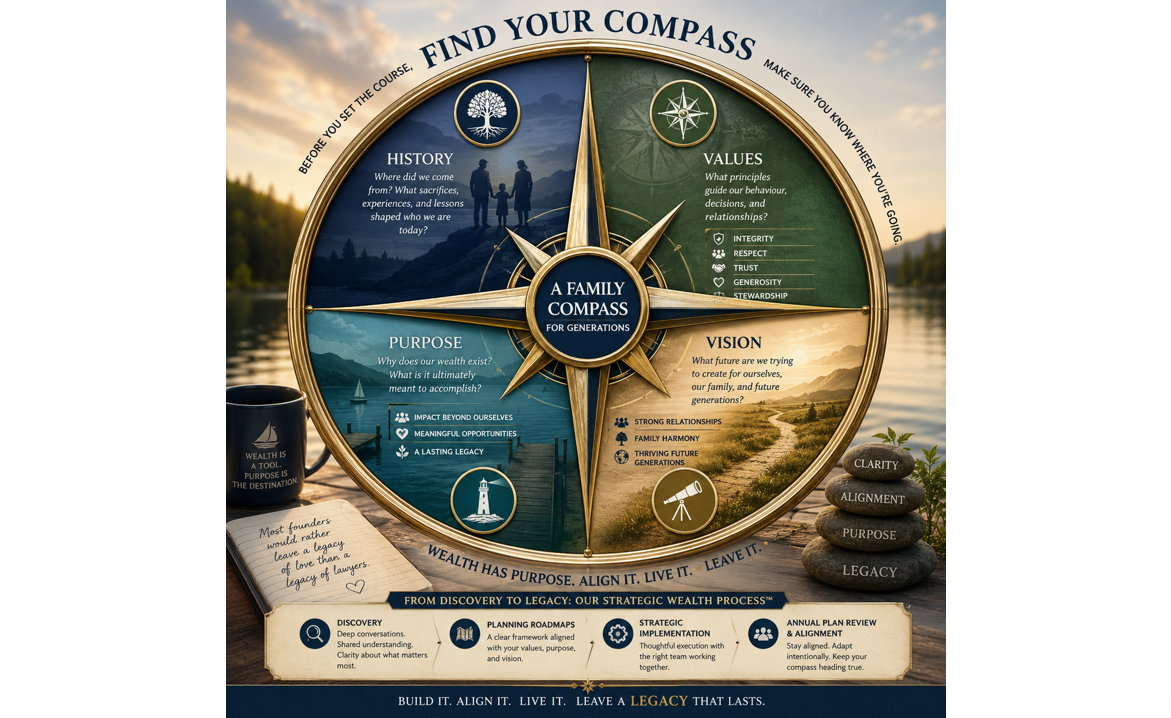

Before you Set the Course, Find Your Compass: Why July May Be the Perfect time to Reflect on What Your Wealth is Meant to Accomplish

Financial independence changes the questions. Once wealth has been built, the focus shifts from accumulation to purpose—what is your wealth meant to accomplish, and what legacy will it create? Summer offers a rare opportunity to step back, reflect on your family's values and vision, and ensure every future decision is guided by a clear sense of direction rather than simply the pursuit of more.

Family Business Leadership: Creating Space for Wise Decisions

Strong family business leadership is about more than guiding daily operations. It requires creating space for meaningful conversations, thoughtful planning, and the development of future leaders. By fostering open communication, sharing values, and investing in the next generation, families can build the clarity, confidence, and alignment needed to strengthen both the business and the relationships that support it for years to come.

Decisions That Last: How Business Owners Can Build Multi-Generational Impact

Taking the time early to engage the next generation in leadership discussions transforms what could be a tense handoff into a shared vision for the business. By mapping out not just the “what” but the “why” behind decisions, you can create alignment and trust that will carry forward for years.

Beyond Net Worth: How Family Stories Build Stronger Generational Wealth

When families avoid conversations about money, stewardship, values, failures, or clarity behind past decisions, future generations are left trying to interpret the silence.

How Financial Fluency Protects Your Business and Family Legacy

Many entrepreneurs delay reviewing their estate plans, shareholder agreements, or tax strategies because planning feels complex or there isn’t enough time. Yet clarity in your finances can prevent misunderstandings, conflict, and costly mistakes, keeping your family and business aligned as you move into 2026.